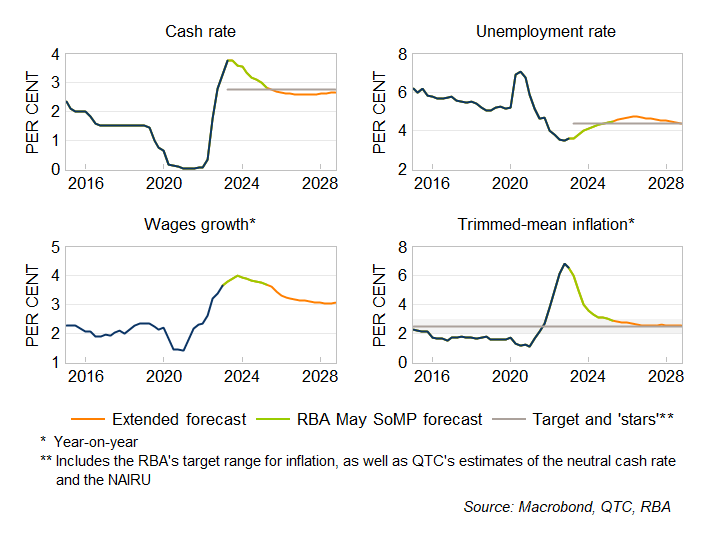

Looking beyond the RBA’s forecast horizon

To assess the risks to the outlook, it is helpful to have a sense of the most likely path for economy and when it could eventually stabilise. Unfortunately, the RBA’s forecasts currently end in mid-2025, a point at which inflation has just reached the top of its target range, the unemployment rate is increasing, and the cash rate is moving lower.

With the RBA’s forecasts too short to make a fulsome assessment of the outlook, I have used a modified version of its MARTIN model to extend the forecasts beyond 2025 (Graph 1).[2] In many respects, these baseline projections could be described as a ‘soft landing’ scenario.[3] The unemployment rate increases, but it remains below the levels seen in the years prior to the pandemic. Wages growth also stabilises at three per cent (which is around its long-run average), while inflation eases towards the middle of the RBA’s target band.

The main issue highlighted by this forecast extension is that the return of inflation to its target is slow. The RBA’s forecasts suggest that inflation could be above its target range for three years, while my forecast extension suggests it could be another 18 months before it reaches the middle of the band. As noted by the RBA Board, this leaves ‘little room for upside surprises’.[4]

Graph 1: Economic conditions are expected to stabilise from around FY 2026-27

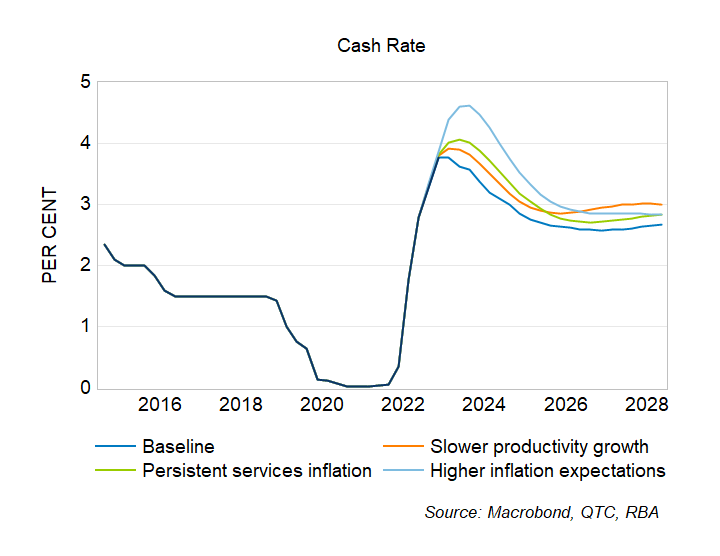

What are the risks to this outlook?

The RBA’s May Board minutes made clear that the cash rate hike in the month was in response to the outlook for inflation and the risk that its return to target could take longer than expected. Notably, the minutes cited several risks that could see inflation remain higher for longer, including (a) services inflation being more persistent than expected, (b) slower-than-expected productivity growth resulting in higher production costs, and (c) the high level of inflation becoming embedded in inflation expectations.

To get a sense of how the realisation of these risks could affect the outlook for inflation and the cash rate, I have constructed the following scenarios using a modified version of the RBA’s MARTIN model (more detail can be found in the appendix).

- Persistent services inflation: The persistence of services inflation across advanced economies appears to be closely related to the ongoing strength in global labour markets.[5] Given this, for this scenario I assume that labour market conditions are more resilient than expected and that this supports a higher level of services inflation.[6]

- Slower productivity growth: The baseline forecasts for inflation assume labour productivity growth returns to 1 per cent by mid-2025. As a downside risk, I have assumed that productivity growth instead only increases to its pre-COVID rate of 0.5 per cent over the next couple of years, before belatedly picking up further.

- Higher inflation expectations: I assume that inflation expectations respond to higher inflation, which results in expectations increasing to slightly above 3 per cent by early 2024. Expectations then gradually decline, reaching the middle of the target band by 2032.

Each of these scenarios results in the cash rate being higher than its baseline (Graph 2). The scenario with ‘slower productivity growth’ has the cash rate remaining unchanged in the near term, while the ‘persistent services inflation’ scenario sees it increase by a further 25 basis points. In both scenarios, cash rate cuts are delayed until the second half of 2024, with rates remaining 20-40 basis points higher than their baseline over much of the forecast horizon.

The ‘higher inflation expectations’ scenario has a noticeably stronger near-term outlook for the cash rate. To break the feedback effect between actual and expected inflation, this scenario sees the RBA increase the cash rate to 4.6 per cent by the end of this year and keep it at this higher level over the first half of 2024.

Graph 2: Each of the scenarios results in a higher profile for the cash rate

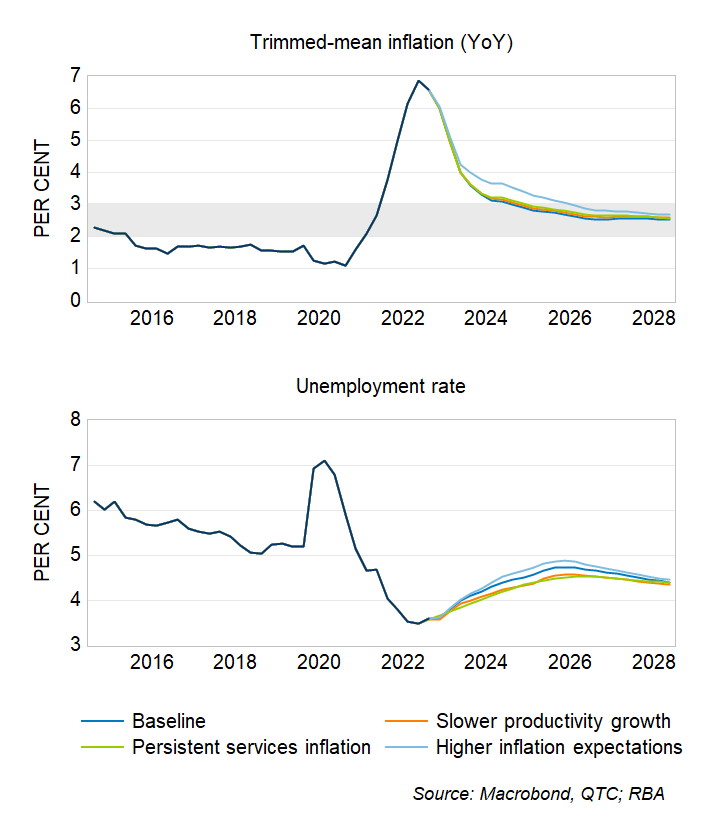

In the first two scenarios, the higher path for the cash rate is enough to offset the upward pressure on inflation, with inflation still reaching the top of its target band around mid-2025 (Graph 3). However, despite a noticeably higher cash rate, the scenario with ‘higher inflation expectations’ sees a much slower return of inflation to its target.

What explains these different outlooks for inflation? In the first two scenarios, higher inflation occurs alongside stronger labour market conditions.[7] This makes the RBA’s cash rate decision relatively straightforward, as higher interest rates address both a stronger outlook for inflation and the unemployment rate. In contrast, in the third scenario, the RBA faces a greater trade-off between addressing higher inflation and maintaining ‘full employment’.[8] This trade-off sees it accept a slower return of inflation to its target in exchange for avoiding even larger increases in the unemployment rate.

Graph 3: Higher inflation expectations could see a much slower return of inflation to its target

What does this mean for monetary policy?

The RBA is paying close attention to the expected timing of inflation reaching its target, with the Board previously noting that inflation returning to the top of the target band any later than mid-2025 would be inconsistent with its mandate. This means that future moves in the cash rate could be quite sensitive to any changes in the outlook for inflation.

The materialisation of any of the risks considered by the RBA Board at its May meeting could see the cash rate remain higher for longer. However, my results suggest that the most costly risk considered by the Board is high inflation becoming embedded inflation expectations. While there are no signs of this happening to date, the RBA may still decide to increase the cash rate further over the coming months as ‘insurance’ against such an outcome. This is a strategy being adopted by its peers around the world such as the US Federal Reserve. Given the global nature of this inflation shock and the desire for central banks to preserve their inflation fighting credentials, the RBA may perhaps follow suit.